Banking embedded is changing how people interact with money. Instead of going to a bank’s website or app, you can now get loans, make payments, or even invest right where you shop or do business online. It’s popping up everywhere, from ride-sharing apps to online stores. This shift is making financial services feel like just another part of your daily routine. It’s a big deal for both consumers and businesses, and it’s only getting bigger.

Key Takeaways

- Banking embedded lets people use financial services directly inside non-bank apps and websites.

- It started with simple things like store cards but now covers payments, loans, and even insurance within everyday platforms.

- This trend is shaking up traditional banks, pushing them to team up with tech companies or risk falling behind.

- APIs, open banking, and the spread of internet access have made banking embedded possible and more common.

- While banking embedded brings convenience and new business opportunities, it also means companies need to be careful about data security and following financial rules.

Understanding The Rise Of Banking Embedded

Defining Embedded Finance: A Seamless Integration

Think about the last time you bought something online. You probably didn’t even think about it, but chances are, you used embedded finance. It’s when financial services, like payments or even loans, are built right into the apps and websites you use every day. You’re not going to a bank’s website to get a loan for that new couch; the furniture store’s website offers it to you right there at checkout. This is the core idea: making financial stuff disappear into the background of other activities. It’s not about banking anymore; it’s about getting what you need, when you need it, without the usual fuss.

The Core Components Powering Embedded Banking

So, how does this magic happen? It’s not just one thing. Several pieces have to work together.

- APIs (Application Programming Interfaces): These are like the digital messengers that let different software talk to each other. They allow a non-financial company to connect to a bank’s systems without needing to build everything from scratch.

- Open Banking: This is a set of rules, especially in places like Europe, that forces banks to share customer data (with permission, of course!) with other companies. It’s like opening up the bank’s vault so others can build cool things on top of it.

- Cloud Computing: This is the behind-the-scenes tech that makes everything scalable and accessible from anywhere. It’s the engine that keeps these integrated services running smoothly.

- Data Analytics: Companies use data to understand what customers need and offer the right financial product at the right time. It’s about being smart with information.

Real-World Examples of Banking Embedded

We see this everywhere now. Take ride-sharing apps – they handle payments, driver payouts, and sometimes even offer loans to drivers, all within the app. Or consider e-commerce platforms that let you pay in installments directly at checkout, thanks to services like Klarna or Affirm. Even accounting software might offer business loans based on your company’s financial data. It’s about convenience, plain and simple. You’re already there, you’re already doing something, and now you can handle your finances without leaving that space.

The Evolution And Impact Of Banking Embedded

Historical Roots of Embedded Financial Services

It’s easy to think embedded banking is some brand-new thing, but honestly, the idea has been around for a while. Think back to when stores offered their own credit cards or simple store credit. You could buy stuff right there, using a financial service tied to the shop. That was the early version, really. The big shift started happening when the internet became a thing, and then smartphones popped up everywhere. Suddenly, it was way easier to connect different systems, especially with things like APIs making it possible for software to talk to each other. Companies like PayPal were early players, putting payment processing right into online stores. They showed how you could make buying things online smoother, paving the way for more complex financial stuff to be tucked into other apps and websites.

Key Milestones in Embedded Banking Growth

At first, embedded finance was mostly about payments. You bought something, and the payment was handled right there. But it grew. Now, you see things like insurance or even investment options popping up inside apps you use for other things. A really big moment was when places like Europe introduced rules called Open Banking, especially PSD2. This basically forced banks to open up their systems so other companies could connect to them. This was huge for embedded banking because it let fintech companies build new financial services on top of what banks already had, and offer them directly to people.

More recently, platforms like Shopify and Stripe have become major players. They don’t just handle payments anymore; they also offer loans or other financial products directly to businesses using their services. It’s a clear sign that embedded finance is getting more sophisticated and covering more ground.

Disruption of Traditional Banking Models

Embedded banking is really shaking things up for the old-school banks. Instead of being the only place people go for money stuff, banks are now part of a bigger picture. They have to figure out how to fit into this new world to stay relevant. A lot of them are teaming up with fintech companies. They use their big, established systems to power the financial features that other companies want to offer. You see this with things like the Apple Card, where Goldman Sachs provides the banking muscle behind the scenes for Apple’s credit card. It shows how banks are adapting, working with others to reach customers in new ways.

Benefits And Challenges Of Banking Embedded

So, what’s the big deal with putting banking services right where people are already doing things online? It turns out there are some pretty sweet advantages, but also a few things to watch out for.

Unparalleled Convenience and Customization

Think about it: no more jumping between apps or websites to pay for something or get a loan. Embedded banking means you can handle financial stuff right inside the app or site you’re already using. It’s like having a bank teller appear exactly when and where you need them, without the waiting room.

- Instant Access: Get loans, make payments, or manage accounts without leaving your current task.

- Personalized Offers: Services can be tailored based on your activity within the platform, making them more relevant.

- Reduced Friction: The whole process becomes smoother, meaning fewer steps and less hassle for you.

This level of convenience is a game-changer for how we interact with money.

New Revenue Streams and Customer Engagement

For businesses that aren’t banks, embedding financial services can be a smart move. It’s not just about making things easier for customers; it can actually make them stick around longer and even bring in extra cash.

- Increased Loyalty: Customers appreciate when their needs are met easily within a familiar environment.

- Additional Income: Businesses can earn fees or interest from the financial services they offer.

- Deeper Insights: Understanding how customers use financial services within the platform can lead to better product development.

Navigating Regulatory Compliance and Data Security

Now, for the tricky part. When you start mixing financial services with other types of business, things get complicated, especially when it comes to rules and keeping data safe. It’s not as simple as just plugging in a new feature.

- Complex Rules: Different countries and regions have specific laws about financial transactions, data handling, and consumer protection. Keeping up with all of them is a big job.

- Protecting Information: Financial data is sensitive. Companies need really strong security measures to prevent breaches and keep customer information private.

- Risk Management: There’s always a risk of fraud or errors. Businesses need systems in place to catch and deal with these issues quickly.

It’s a balancing act, for sure. You want to offer all these great, convenient services, but you absolutely have to do it the right way, following all the rules and keeping everyone’s information secure. It requires careful planning and ongoing attention.

Technological Enablers For Banking Embedded

So, how does all this embedded banking stuff actually work? It’s not magic, though sometimes it feels like it. There are a few key pieces of tech that make it all possible, really.

The Crucial Role of APIs

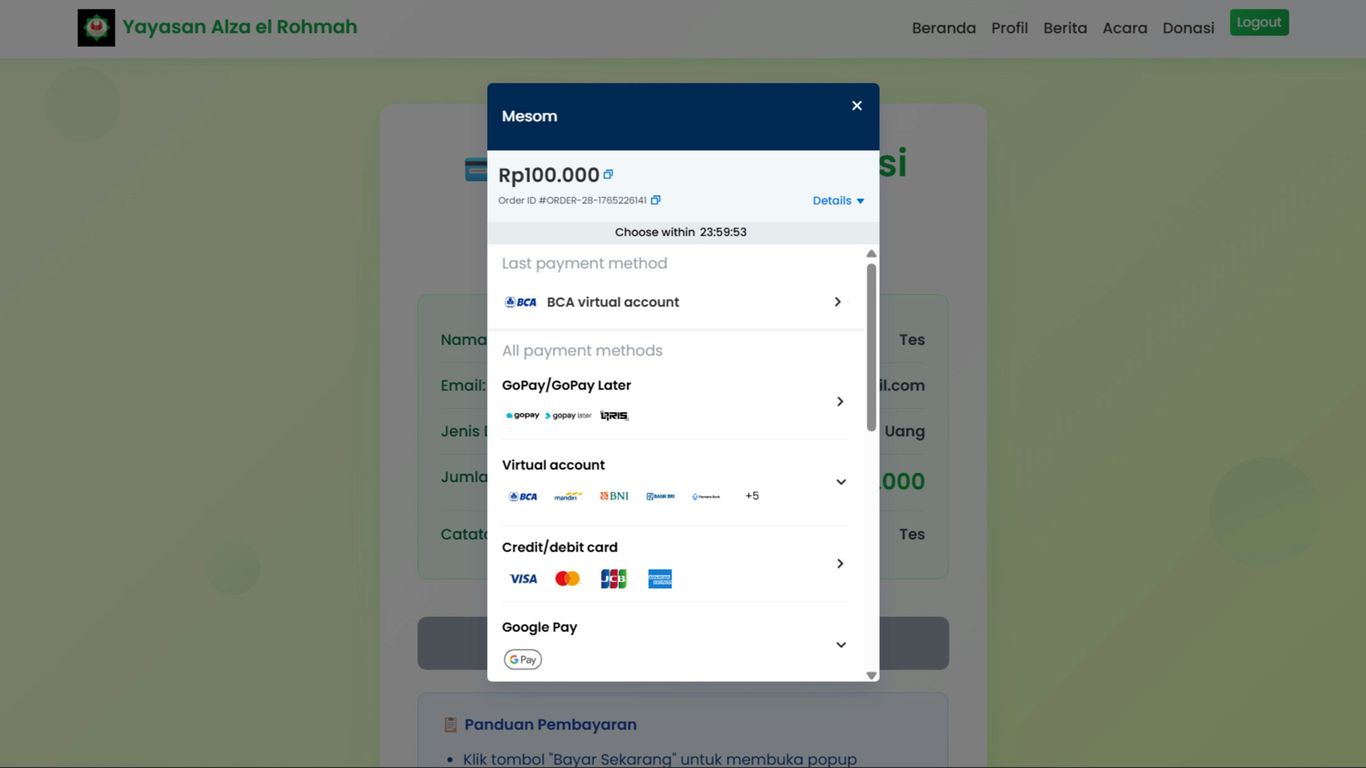

Think of APIs, or Application Programming Interfaces, as the messengers between different software programs. In embedded banking, they’re super important. They let a company’s app or website talk directly to a bank’s systems. So, when you see a ‘buy now, pay later’ option on a shopping site, it’s an API that’s connecting the store to a lender. This lets you get approved for credit right there, without leaving the checkout page. It’s like having a direct line from the store to the bank’s loan department, making things quick and easy.

Leveraging Open Banking Initiatives

Open banking is a big deal here. It’s basically a set of rules that makes banks share their data (with your permission, of course) with other companies, usually through those APIs we just talked about. This has really opened the door for innovation. Fintech companies can now build cool new financial tools and services that plug right into other apps. For example, your budgeting app might use open banking to pull your transaction history from your bank so it can give you personalized tips. It’s all about making financial information more accessible and useful.

The Impact of Ubiquitous Internet Connectivity

And of course, none of this would be happening on a large scale without the internet. Pretty much everyone has a smartphone and internet access these days, right? This widespread connectivity means businesses can offer financial services to a massive audience, anytime, anywhere. Whether you’re applying for a small loan on your phone while waiting for a bus or checking your investments from your couch, the constant internet connection makes these embedded financial actions happen in real-time. It’s the foundation that lets all these other technologies work together smoothly.

The Future Landscape Of Banking Embedded

Transforming Consumer and Business Relationships

So, where is all this headed? It looks like banking is going to become even more woven into the fabric of our digital lives. Think about it: instead of going to a bank’s website or app, you’ll likely handle financial stuff right where you’re already doing things. For consumers, this means less hassle. You might buy something online and get a loan offer on the spot, or manage your investments within a social media app. It’s all about making things super convenient.

For businesses, this opens up a whole new world. They can offer financial products directly to their customers, which builds stronger relationships. Imagine a small business owner getting a loan directly through their accounting software, or a freelance platform offering insurance to its users. This integration means businesses can keep customers engaged and potentially create new income streams. It’s a big shift from how things used to be, where banks were separate entities.

Driving Financial Inclusion Through Integration

One of the really exciting parts of embedded banking is its potential to help people who haven’t always had easy access to financial services. When banking functions are built into everyday apps and platforms, they become available to more people, no matter where they live or what their income is.

Here’s how it can help:

- Reaching Underserved Areas: People in rural areas or developing countries might not have local bank branches. Embedded finance can bring services to them through their mobile phones.

- Lowering Barriers: Traditional banking can sometimes feel intimidating or require a lot of paperwork. Embedded options are often simpler and more straightforward, making them easier for newcomers to use.

- Tailored Products: Services can be designed to fit specific needs. For example, a farmer might get a loan through an agricultural app that understands their seasonal income, something a big bank might not easily do.

This move towards more accessible finance could really change things for millions.

Redefining Global Commerce and Finance

Looking ahead, embedded banking is set to change how we buy, sell, and manage money on a global scale. It’s not just about convenience anymore; it’s about creating a more connected and efficient financial world.

We’re likely to see:

- More Sophisticated Integrations: Beyond just payments and loans, expect to see insurance, investments, and even complex financial planning tools embedded into various platforms.

- New Business Models: Companies that aren’t banks today could become major players in financial services by embedding these capabilities.

- Global Reach: As technology improves, embedded finance can help bridge gaps in international trade and payments, making it easier for businesses to operate across borders.

The total value of financial transactions handled through embedded finance is projected to grow significantly, moving from trillions of dollars to even higher figures in the coming years. This trend suggests a future where financial services are not a destination, but a natural part of any digital interaction.

Conclusion

Embedded banking is changing the way we think about money and financial services. Instead of going to a bank or using a separate app, people can now access things like payments, loans, or insurance right where they shop or do business online. This shift is making things easier and faster for everyone—consumers and companies alike. Of course, there are still some bumps in the road, like making sure everything is safe and follows the rules. But as more businesses and tech companies get involved, it looks like embedded banking is here to stay. It’s not just a trend; it’s becoming the new normal for how we handle our finances in everyday life.

Frequently Asked Questions

What is embedded banking?

Embedded banking is like having banking services pop up right where you need them, like when you’re shopping online or using an app. Instead of going to a separate bank website, you can do things like get a loan or pay for something without leaving the app or website you’re already using. It makes banking feel like a natural part of what you’re already doing.

How is embedded banking different from regular banking?

Regular banking usually means you have to go to a bank’s branch or website to do your banking. Embedded banking is different because it brings those banking services directly to you, inside other apps and websites you use every day. Think of it as banking coming to you, instead of you having to go to banking.

What are some examples of embedded banking?

A great example is when you buy something online and can choose to pay later with a service like ‘buy now, pay later’ right at checkout. Another is when a ride-sharing app lets drivers manage their earnings and even get loans directly within the app. It’s about financial tools being part of the experience.

Why is embedded banking becoming so popular?

It’s popular because it’s super convenient! People don’t have to switch between different apps or websites to manage their money. It also helps businesses offer more services to their customers, and it can even help people who don’t normally use banks get access to financial tools.

What technology makes embedded banking possible?

The main technology is called APIs, which are like digital messengers that let different software talk to each other. Also, ‘open banking’ rules allow banks to share information (with your permission!) so other companies can build cool new services. And, of course, having the internet everywhere makes it all work smoothly.

Are there any downsides to embedded banking?

Yes, there can be. Companies offering these services need to be very careful about keeping your personal and financial information safe. They also have to follow strict rules and laws, which can be complicated. Making sure everything is secure and legal is a big challenge.